")

With tax season in full swing for CPAs, the numbers can become jumbled, social interaction few and far between, and little to no time for additional questions you may have outside of your tax return. Over the years, I’ve noticed clients tend to have a lot of the same questions on their mind. Let’s look at three of the more commonly asked questions.

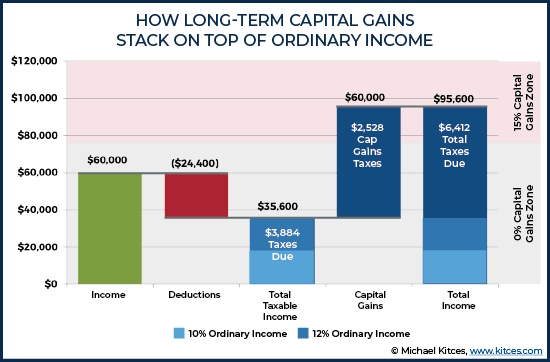

- Can capital gains push me into a higher tax bracket?

A commonly used answer for tax questions applies here: it depends. Short-term capital gains (gains from an asset that you owned for a year or less) are treated as ordinary income. Effectively, this means short-term capital gains are treated the exact same as wages and can push you into a higher tax bracket. Short-term capital gains do not receive the same preferential tax treatment as long-term capital gains.

If you own capital assets for greater than one year, they are subject to long-term capital gains. Long-term capital gains have their own tax brackets of 0%, 15%, and 20%. After your ordinary income is calculated, the long-term capital gains are stacked on top to determine their tax rate. While your ordinary income has an impact on the tax rate of your long-term capital gains, your long-term capital gains (no matter the amount) cannot change the tax rate of your wages, short-term gains, business income, etc.

- What can be done about my tax bill after December 31st?

The shock of owing more in taxes than you were anticipating can ruin your day, week or even your whole year. After December 31st, most of the hay is already in the barn as they say. However, below are a few things that can be done to make sure the bill is as low as possible.

Maximize Contributions to Eligible Accounts – Taxpayers can contribute to IRAs and HSAs by April 15th and SEP IRAs and Solo 401(k)s by October 15th for a deduction in the prior year if eligible.

Make Payments on Time – The last estimated quarterly tax payment for any given year is due January 15th of the following year. Even if the first three payments were not made, making a payment by January 15th could help cut down on significant penalties and interest. In the same vein, if you weren’t required to make estimated payments in the prior year but will need an extension and owe money for the given tax year, paying the estimated tax bill with your extension can generate significant savings.

Ensure Proper Elections are Made – Specifically when it comes to business property, there have been several changes to bonus depreciation. Evaluating whether to use Section 179 or bonus depreciation for depreciable assets can result in more expenses and less taxes.

- When is it better to file married filing separately?

Unfortunately, there is not a specific threshold or number to look for that will guarantee married filing separately will be better than filing jointly. The only way to know for sure is preparing the tax return both ways to determine the tax liability. In general, the most common reason to file separately would be if one spouse had large amounts of medical bills and needed the lower AGI to get over the threshold for deductibility, if one spouse is on an income-driven student loan repayment plan, or the spouses have separate finances or are going through a divorce.

The tax code is written to give the edge to married filing jointly as certain credits and deductions are disallowed under the married filing separately filing status. Married filing separately creates an additional burden on the IRS having to process an additional return, check it against another return and make sure all numbers are accurate. To tip the scales in married filing jointly’s status even further, if you live in a community property state (like Louisiana) all community income (including all earned income for the year) must be split 50/50 on the married filing separately returns.

As you prepare your taxes, we hope this information helps clarify what are typically the most vexing tax questions. While we hope this is educational, the above information is to be used as a guide, and we highly recommend contacting your CPA or us to discuss how the information applies to your personal situation.